Global Market Snapshot:

U.S. :

The upcoming week on Wall Street shows that a robust performance in 2023 may keep US stocks on the path for 2024 gains.

The substantial increases witnessed in the U.S. stock market during 2023 may offer support for equities in the coming year, drawing insights from historical patterns.

As 2023 ends, investors have ample reason for celebration, as the S&P 500 concludes the year with a remarkable gain exceeding 24%, and the Dow wraps up near a record high. The alleviation of inflationary pressures, a robust economy, and the anticipation of lower interest rates have uplifted investors, particularly during the final two months of the year.

On the final trading day of 2023, the primary S&P 500 index showed a marginal decrease, concluding the year with an impressive 24.2% gain. Meanwhile, the Dow Jones Industrial Average achieved a notable rise of over 13% throughout the year, and the Nasdaq experienced a remarkable surge of 43%, propelled by the successes of major technology firms like Nvidia, Amazon, and Microsoft.

The rally that started in November played a role in extending market gains beyond the significant technology firms. Additionally, investor sentiment received a boost from the Federal Reserve’s December announcement, outlining its intention to implement three interest rate cuts in 2024.

The majority of major indexes successfully recovered from the setbacks experienced in the challenging year of 2022. Although smaller company stocks saw a late rally, they were able to mitigate a significant portion of their losses from the previous year. The Russell 2000 index concluded 2023 with a notable 15.1% gain, rebounding from a 21.6% decline in 2022.

Investors Hoping for more of the same in 2024.

The robust performance of the US markets throughout 2023 has surprised many investors and commentators, who are optimistic for a continuation of this trend into the new year. The Nasdaq witnessed a remarkable surge of $7 trillion in the past 12 months, primarily fuelled by AI-heavy stocks, while the S&P and Dow are approaching record highs. Investors are anticipating a potential final ‘Santa Rally’ in the first few days of the new year, hoping for technical breakthroughs that could propel indices into new, higher ranges for Q1 2024. Nevertheless, some skeptics express concerns. Recent developments in the bond markets, effectively acting as rate cuts in the US, raise concerns about inflationary pressures. Moreover, there is apprehension that the rapid ascent of equities into overbought territory might have been too hasty, paving the way for potential significant corrections that could dampen the enthusiasm for the new year.

Europe:

The European stock market has been exceptionally impressive in 2023, showcasing a narrative of resilience and notable success that has surpassed initial skepticism.

The Euro Stoxx 50 index, a crucial gauge for Europe’s major corporations, has witnessed a notable year-to-date surge of 19%, recovering from the 12% decline experienced in 2022.

Taking the lead in terms of performance within the Euro Stoxx 50 are some of Europe’s most distinguished entities, demonstrating substantial gains that have pleasantly surprised investors.

European stocks conclude 2023 with a 12.64% increase following gains on the final trading day.

On Friday, the Stoxx closed the day with a provisional 0.1% increase, as nearly all sectors saw gains in light trading. London markets closed early, with the FTSE 100 in positive territory while the FTSE 250 experienced a decline.

The DAX in Germany has experienced an almost 20% increase throughout 2023, despite the country’s challenging economic conditions. In the same period, France’s CAC 40 and the UK’s FTSE 100 have recorded gains of 16.4% and 3.64%, respectively.

Asia:

Asian markets conclude the final trading day of 2023 with modest decreases, while Chinese stocks experience a slight uptick fuelled by the ongoing ascent of technology firms.

On the concluding trading day of 2023, markets in the Asia-Pacific region witnessed declines across the board, except for China, where stocks, particularly those of the country’s technology firms, continued their upward trajectory.

On Thursday, Xiaomi, the Chinese consumer electronics company, outlined its intentions to venture into China’s crowded electric vehicle market. By afternoon trading, the company’s Hong Kong shares had declined by over 4%.

Although the yen has significantly weakened against the U.S. dollar, there are projections that it will strengthen in 2024. However, this potential strengthening is not anticipated to hurt equities.

Despite a more than 2% rally in the previous session, both China and Hong Kong indexes were poised to be the most significant percentage decliners for the year among major Asia-Pacific markets.

The CSI 300 index in China has experienced an 11.8% decline for the year, whereas the Hang Seng has witnessed a 14% plunge in 2023.

Japan’s Nikkei 225, concluding at 33,464.17 with a marginal 0.22% decline, concluded the year as Asia’s best-performing market, boasting gains of over 28%. The broader Topix, finishing 0.19% higher at 2,366.39, demonstrated a substantial increase of over 25% throughout 2023.

2024 Investment Outlook:

In 2024, investors will need to make careful decisions, closely monitoring monetary policy, to navigate potential challenges and identify opportunities in a world characterized by moderating yet persistently high inflation and decelerating global growth.

The notion that central banks will smoothly transition to lower inflation levels has already been factored into asset prices, indicating limited room for further valuation increases. However, income investing is expected to thrive in 2024, with Morgan Stanley Research strategists identifying promising opportunities in high-quality fixed income, government bonds in developed markets, and other areas.

Serena Tang, Chief Global Cross-Asset Strategist at Morgan Stanley Research, emphasizes the importance of central banks striking the right balance between gradual tightening and swift easing. She suggests that for investors, 2024 will be focused on navigating carefully and identifying subtle opportunities in the markets that can yield positive returns.

Navigating the final phase of inflation is expected to result in a deceleration of growth, particularly in the U.S., Europe, and the UK. Simultaneously, China’s modest growth is anticipated to impact emerging markets, with a potential risk of the country’s economy being drawn into a broader debt-deflation spiral, affecting Asia and beyond. Morgan Stanley foresees that China will avert the worst-case scenario, and policymakers in the U.S. and Europe will initiate rate cuts in June 2024, enhancing the macroeconomic outlook for the latter part of the year.

During 2023, equity markets demonstrated robust performance, rebounding from the recession fears that influenced the trough in October 2022, showcasing greater resilience than analysts had anticipated. Nevertheless, 2024 is expected to unfold as a “tale of two halves,” characterized by a cautious first half transitioning into stronger performance in the latter part of the year.

In the initial half of 2024, strategists advise investors to exercise patience and be discerning. Elevated risks to global growth, influenced by monetary policy, persist, and challenges in earnings may endure until the early part of 2024 before a rebound materializes. Historically, global stocks tend to experience a decline in the three months preceding a new phase of monetary easing, as risk assets factor in expectations of decelerated growth. Should central banks adhere to their schedule of initiating rate cuts in June, global equities might witness a devaluation in the early months of the year.

2024 Key Stock Market Outlook Key Takeaway:

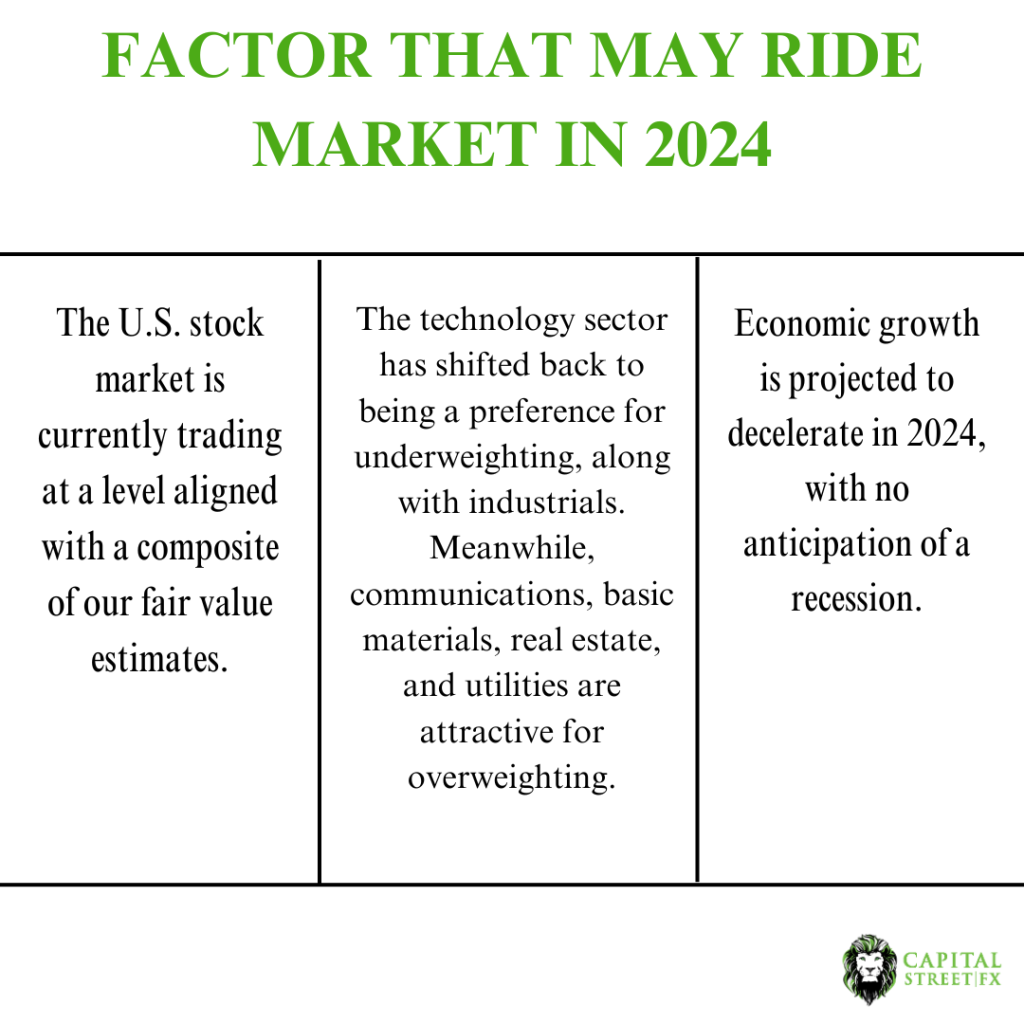

- The U.S. stock market is currently trading at a level aligned with a composite of our fair value estimates.

- Value stocks and small-cap stocks continue to be available at appealing discounts.

- The technology sector has shifted back to being a preference for underweighting, along with industrials. Meanwhile, communications, basic materials, real estate, and utilities are attractive for overweighting.

- Economic growth is projected to decelerate in 2024, with no anticipation of a recession.